What Is A Mortgage Loan And How Does It Work?

A mortgage loan is a type of loan specifically used to purchase real estate. It is a long-term debt where the borrower agrees to pay back the loan amount with interest over a set period of time, usually between 15 to 30 years. The loan is secured by the property itself, meaning that if the borrower fails to repay the loan, the lender has the right to seize the property through a process known as foreclosure.

Mortgage loans are a fundamental part of the housing market, enabling millions of people to buy homes who might not have the full amount of cash to pay upfront. For most people, purchasing a home is one of the largest financial commitments they’ll ever make. Understanding how mortgage loans work is crucial for making informed decisions about home ownership and personal finances.

In this article, we’ll delve into the details of mortgage loans, how they function, their types, and important considerations to keep in mind. Additionally, we’ll provide answers to common questions, a comprehensive conclusion, and key takeaways.

Key Takeaways:

- A mortgage loan is a secured loan used to buy property, where the property acts as collateral.

- Mortgage loans come in various forms, including fixed-rate, adjustable-rate, FHA, VA, and jumbo loans.

- Your credit score, income, down payment, and debt-to-income ratio are key factors in securing a mortgage loan.

- It’s essential to understand closing costs, PMI, and other fees associated with mortgages.

- Refinancing is an option if you want to adjust the terms of your existing mortgage to suit your financial needs.

How Does a Mortgage Loan Work?

A mortgage loan works by allowing you to borrow money from a lender, typically a bank or credit union, to buy a home or property. The property acts as collateral for the loan, which means that if you fail to repay the loan, the lender can take possession of the property.

Here’s how the process typically works:

- Loan Application: You apply for a mortgage loan by providing financial information, such as your income, credit history, and details about the property you intend to purchase. The lender will use this information to assess your ability to repay the loan.

- Pre-Approval: Once the lender reviews your application, they may offer you a pre-approval, which indicates the loan amount you qualify for. Pre-approval helps in narrowing down the property search because it tells you how much house you can afford.

- Choosing the Right Loan Type: There are various types of mortgage loans, such as fixed-rate, adjustable-rate, and government-backed loans. Each comes with different terms, interest rates, and repayment structures.

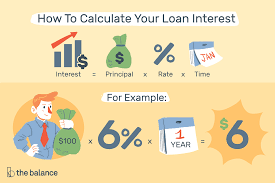

- Interest Rates: The interest rate on your mortgage is the cost of borrowing the loan. It can either be fixed (stays the same over the life of the loan) or adjustable (can fluctuate over time). The rate significantly impacts your monthly payments and the total cost of the loan.

- Down Payment: Typically, lenders require a down payment, which is a percentage of the home’s purchase price. It usually ranges from 3% to 20%, depending on the loan type and your creditworthiness. A higher down payment can reduce your monthly payments and help you avoid private mortgage insurance (PMI).

- Monthly Payments: Once you are approved for the loan, you make monthly payments to the lender. These payments cover the loan principal (the amount you borrowed), the interest (the cost of borrowing), and possibly taxes and insurance. Over time, a larger portion of your monthly payment goes toward the principal, while the interest decreases.

- Repayment Period: Most mortgage loans are structured for a long repayment period, typically 15, 20, or 30 years. The longer the loan term, the lower your monthly payments, but the more interest you pay over the life of the loan.

- Amortization: Mortgages are typically amortized, meaning that the loan is paid off gradually over time. Early payments are mostly applied to interest, but as the loan balance decreases, more of your monthly payment goes toward the principal.

- Closing Costs: In addition to the down payment, there are also closing costs, which include fees for appraisals, inspections, title searches, and paperwork. These costs can range from 2% to 5% of the loan amount.

Types of Mortgage Loans

There are several types of mortgage loans, each with its own characteristics, terms, and benefits. Understanding these options will help you choose the best one for your financial situation.

- Fixed-Rate Mortgages (FRM):

With a fixed-rate mortgage, the interest rate remains the same for the entire life of the loan. This predictability makes it easier for homeowners to budget their monthly payments. Common fixed-rate terms are 15 and 30 years. A 30-year fixed-rate mortgage is the most common option, providing lower monthly payments but higher total interest costs over time. - Adjustable-Rate Mortgages (ARM):

An adjustable-rate mortgage has an interest rate that changes periodically based on market conditions. Initially, ARMs often have lower interest rates than fixed-rate loans, making them attractive to homebuyers looking to save money in the early years. However, the rate can increase, leading to higher monthly payments over time. The most common ARM is the 5/1 ARM, where the interest rate is fixed for the first 5 years, then adjusts annually. - FHA Loans:

Federal Housing Administration (FHA) loans are government-backed mortgages designed for low-to-moderate-income borrowers. FHA loans typically require a lower down payment (as low as 3.5%) and have more lenient credit score requirements, making them a good option for first-time homebuyers. - VA Loans:

Veterans, active-duty military members, and their families may qualify for VA loans, which are backed by the U.S. Department of Veterans Affairs. VA loans require no down payment or private mortgage insurance (PMI), making them a great option for those who qualify. - USDA Loans:

United States Department of Agriculture (USDA) loans are available for rural and suburban homebuyers who meet income requirements. These loans require no down payment and offer competitive interest rates, making them an excellent option for buyers in eligible areas. - Jumbo Loans:

A jumbo loan is a type of mortgage loan that exceeds the conforming loan limits set by the Federal Housing Finance Agency (FHFA). These loans are often used for purchasing high-value homes. Jumbo loans typically come with higher interest rates and stricter credit requirements.

Factors Affecting Mortgage Loan Approval

Several factors influence whether or not you will be approved for a mortgage loan, and how favorable the terms will be. These factors include:

- Credit Score: Your credit score is one of the most important factors in determining whether you qualify for a mortgage loan. A higher score indicates to lenders that you are a lower risk, making it easier to get approved and secure better interest rates.

- Income and Employment History: Lenders want to know that you have a reliable income and a steady job. This helps them assess your ability to make regular mortgage payments. Lenders typically prefer a debt-to-income (DTI) ratio of less than 36%.

- Down Payment: A larger down payment can increase your chances of being approved for a loan, as it reduces the lender’s risk. It also shows that you are financially responsible and committed to the purchase.

- Property Appraisal: Before approving a loan, the lender will require a property appraisal to determine its market value. The appraisal helps ensure that the loan amount is in line with the property’s worth.

- Debt-to-Income Ratio (DTI): Lenders use your DTI ratio to measure your monthly debt obligations in relation to your income. A lower DTI ratio indicates that you are more likely to manage your mortgage payments successfully.

Additional Considerations for Mortgage Loan Borrowers

While the initial steps of applying for a mortgage may seem straightforward, there are many factors you should consider to ensure you’re making the best possible decision for your long-term financial health. It’s not just about the type of loan you choose, but also about ensuring that the loan fits your personal circumstances and broader financial goals.

Understanding Interest Rates

Interest rates are one of the most critical factors in determining the total cost of your mortgage. Even a small difference in the interest rate can significantly impact the total amount you pay over the life of the loan. For example, a 1% difference in the interest rate on a $200,000 30-year loan could add tens of thousands of dollars to the cost of your mortgage over its lifetime.

- Fixed-Rate Mortgages (FRMs): A fixed-rate mortgage offers stability since your interest rate remains unchanged for the entire term of the loan. This can be ideal for people who prefer predictability in their monthly payments. However, it often comes with a slightly higher interest rate than the initial rate offered on adjustable-rate mortgages (ARMs).

- Adjustable-Rate Mortgages (ARMs): An ARM typically offers a lower interest rate during the initial years of the loan. However, after the fixed-rate period expires (usually 5, 7, or 10 years), the rate may adjust annually based on market conditions. For borrowers who plan to sell or refinance within the first few years of the loan, an ARM can be an appealing option. However, it comes with the risk of rising interest rates in the future, potentially leading to higher monthly payments.

Choosing the Right Mortgage Term

The term length of your mortgage is another important decision. Most people default to the 30-year mortgage, but it’s not always the best choice.

- 15-Year Mortgage: A 15-year fixed-rate mortgage allows you to pay off your home more quickly, and you’ll save a significant amount on interest payments over the life of the loan. However, the monthly payments are generally higher compared to a 30-year mortgage. This option may be ideal for those who want to own their home outright in a shorter period and can afford the higher payments.

- 20-Year Mortgage: A 20-year fixed-rate mortgage strikes a balance between the 15- and 30-year options. You’ll still be able to pay off the loan faster than a 30-year mortgage, but the monthly payments will be more manageable.

- 30-Year Mortgage: A 30-year fixed-rate mortgage is the most common and offers the lowest monthly payments. However, over time, you’ll pay more in interest compared to the shorter-term loans. It’s often chosen by borrowers who want lower monthly payments to keep their budget flexible or who are purchasing a more expensive home.

Additional Fees and Costs in a Mortgage

Aside from the interest rate, there are other costs associated with obtaining a mortgage. These include:

- Private Mortgage Insurance (PMI): If your down payment is less than 20%, you may be required to pay for PMI. This protects the lender in case you default on the loan. PMI typically costs between 0.3% to 1.5% of the original loan amount annually. You can avoid PMI by saving up for a larger down payment or opting for a government-backed loan like an FHA loan, which may allow for lower down payments without PMI.

- Homeowner’s Insurance: Most lenders require borrowers to have homeowner’s insurance to protect the property in case of damage. The cost of insurance can vary significantly based on your location, the value of your home, and the type of coverage you select.

- Property Taxes: Property taxes are another ongoing cost that comes with homeownership. These taxes are typically paid annually or semi-annually and are based on the assessed value of your property. Lenders often collect property taxes along with your monthly mortgage payment through an escrow account.

- Closing Costs: These are fees that are paid at the closing of the mortgage transaction and can add up to 2% to 5% of the total loan amount. Closing costs can include title fees, appraisal costs, home inspections, attorney fees, and more. It’s essential to review these costs ahead of time to avoid surprises.

What Is an Escrow Account?

An escrow account is a special account held by your lender to pay certain property-related expenses on your behalf. This includes property taxes, homeowner’s insurance premiums, and sometimes private mortgage insurance (PMI). Each month, your lender will collect a portion of these expenses as part of your mortgage payment, and then they will pay the appropriate parties on your behalf.

An escrow account can provide peace of mind, as it ensures that you are always up-to-date with property tax and insurance payments. However, it can also increase your monthly mortgage payment, so it’s essential to account for this in your budgeting.

Refinancing Your Mortgage

As your financial situation changes or interest rates fluctuate, refinancing your mortgage can be an attractive option. Refinancing involves replacing your existing mortgage with a new one, typically at a lower interest rate or with different terms. This can help you save money on interest, lower your monthly payments, or pay off your mortgage more quickly.

When refinancing, it’s important to consider factors such as closing costs, the length of time you plan to stay in your home, and whether the savings from refinancing outweigh the costs.

The Role of a Mortgage Broker vs. Direct Lenders

When seeking a mortgage loan, you have two primary options for securing the best deal:

- Mortgage Brokers: A mortgage broker acts as an intermediary between you and potential lenders. Brokers have access to multiple lenders and can help you find the best mortgage rate and terms for your situation. They can be particularly useful if you’re not sure where to start, or if you have a unique financial situation that requires some expertise.

- Direct Lenders: Direct lenders, such as banks, credit unions, or online lenders, provide mortgage loans directly to borrowers. Working with a direct lender can be more streamlined since you’re dealing with just one entity. You may also benefit from lower fees and better customer service, but it limits your options to that specific lender’s offerings.

Also Read :-Do I Qualify for Federal Student Loan Forgiveness?

Conclusion

A mortgage loan is a significant financial commitment that plays a vital role in enabling homeownership for millions of people. Understanding how mortgage loans work, the types available, and the factors influencing your loan approval can help you make more informed decisions when purchasing a home. With the right information, planning, and strategy, you can navigate the home loan process with confidence and secure the best terms for your financial situation.

FAQs

- What is the minimum credit score required for a mortgage loan?

The minimum credit score for a conventional mortgage is typically around 620. However, government-backed loans like FHA and VA loans may accept lower scores. - Can I get a mortgage loan with no down payment?

Yes, certain loan programs like VA loans and USDA loans allow you to buy a home with no down payment. However, other programs may require a minimum down payment. - What is PMI and when is it required?

Private Mortgage Insurance (PMI) is typically required if your down payment is less than 20%. PMI protects the lender in case you default on the loan. - What happens if I miss a mortgage payment?

Missing a mortgage payment can result in late fees, damage to your credit score, and eventually foreclosure if payments are not made for an extended period. - Can I refinance my mortgage loan?

Yes, refinancing allows you to replace your current mortgage with a new one, often with better terms, such as a lower interest rate. It can help lower monthly payments or reduce the loan term. - What is an escrow account in a mortgage?

An escrow account is a special account that holds funds for property taxes and insurance premiums. Your lender may require you to pay into the escrow account as part of your monthly mortgage payment. - What are closing costs?

Closing costs are fees associated with finalizing the mortgage transaction. These can include lender fees, title insurance, appraisals, and inspections, typically ranging from 2% to 5% of the loan amount.