Investing is an essential part of personal finance, but how you invest can make a significant difference in your wealth-building journey. Among the most popular investment strategies are Systematic Investment Plan (SIP) and Lump Sum Investment. Both have their merits, but the better option often depends on your financial goals, risk tolerance, and market conditions. So, which should you choose — SIP or lump sum?

Key Takeaways

SIP is ideal for beginners, regular savers, and volatile markets.

Lump sum works well in bullish markets and with large surplus funds.

Taxation rules are the same for both, depending on the fund type and holding period.

Combining SIP and lump sum can help balance returns and risk.

Long-term perspective and consistency are more important than the mode of investment.

What Is SIP (Systematic Investment Plan)?

Understanding SIP

A Systematic Investment Plan (SIP) is a disciplined investment strategy where you invest a fixed amount regularly (monthly or quarterly) into mutual funds or other investment instruments. SIPs are ideal for salaried individuals or those with a steady income stream.

Rupee cost averaging: SIPs average out the purchase cost over time.

Compounding benefits: Over time, returns compound, boosting your wealth.

Lower entry barrier: You can start SIPs with as little as ₹500 or $10.

What Is Lump Sum Investment?

Understanding Lump Sum Investment

Lump sum investment refers to investing a large amount of money at one go. This method is usually preferred by those who have received bonuses, inheritance, or saved up a considerable corpus.

Key Features of Lump Sum Investment

One-time investment: A large amount is invested upfront.

Market timing: Ideal when markets are at lower levels.

Higher initial exposure: Potential for faster returns in bullish markets.

Requires significant capital: Typically suits those with surplus cash.

How Does SIP Compare with Lump Sum?

SIP vs Lump Sum: A Side-by-Side Comparison

Feature

SIP

Lump Sum

Investment Type

Regular, periodic

One-time, large amount

Risk Exposure

Lower risk, gradual exposure

Higher risk, full exposure

Market Timing

Not critical

Crucial for maximum returns

Affordability

Suitable for small investors

Requires large capital

Compounding Effect

Gradual but consistent

Starts immediately

Ideal For

Salaried individuals

Investors with windfall income

When Should You Choose SIP?

1. If You Have a Steady Income

SIPs are perfect for salaried individuals or those earning regular income. You can invest a portion of your salary every month without straining your finances.

2. If You Are a Beginner

For beginners, SIPs reduce the risk of market volatility. You don’t need to understand complex market trends; just stay consistent.

3. If You Want Financial Discipline

SIPs inculcate a habit of regular saving and investing. Over time, this discipline can build a substantial corpus.

When Should You Choose Lump Sum Investment?

1. If You Have Surplus Funds

Lump sum is ideal if you receive a large sum — like a bonus, property sale, or retirement corpus — and want to invest it for long-term goals.

2. When the Market is Down

Investing a lump sum during market downturns can yield higher returns when the market rebounds.

3. If You Can Handle Market Volatility

Experienced investors who understand market timing and volatility may prefer lump sum for quicker returns.

What Are the Tax Implications?

SIP Taxation

Equity Mutual Funds: Gains held for more than 1 year are long-term and taxed at 10% (if gain > ₹1 lakh).

Debt Funds: Gains after 3 years are taxed at 20% with indexation.

Each SIP installment is treated as a separate investment for taxation.

Lump Sum Taxation

Follows the same rules as SIP regarding fund type.

Since the investment is made at once, calculating holding period and gains is simpler.

How Do Market Conditions Affect SIP and Lump Sum?

SIP in Volatile Markets

SIPs thrive in volatile markets. When prices drop, you buy more units; when prices rise, you buy fewer. This balances out the overall cost — known as rupee cost averaging.

Lump Sum in Bullish Markets

In a strong bull market, lump sum can generate high returns quickly. But if markets crash post-investment, losses can be significant.

Can You Combine SIP and Lump Sum Strategies?

Yes! Many investors use a hybrid approach:

Start with a lump sum, then follow it up with SIPs.

Split a large amount into smaller SIPs over 6–12 months (called STP – Systematic Transfer Plan).

This combination balances market timing risk and disciplined investing.

Which Option Has Better Historical Returns?

While historical returns vary, studies often show that lump sum investments outperform SIPs when the market trends upward steadily. However, SIPs perform better during volatile or bearish phases, reducing risk over time.

Case Study:

Imagine you invest ₹1,20,000:

Lump Sum: Invest ₹1,20,000 on January 1.

SIP: Invest ₹10,000 monthly for 12 months.

If the market rises consistently, lump sum will outperform. If the market is volatile or falling, SIP will yield better average returns.

There’s no one-size-fits-all answer in the SIP vs lump sum debate. It all depends on your financial goals, market conditions, and risk appetite. If you’re new to investing or have a regular income, SIPs provide a safe, disciplined, and steady approach. If you understand the market and have surplus funds, a lump sum investment can offer higher returns in a favorable market.

FAQs

1. Is SIP better than lump sum in a falling market?

Yes, SIPs work better in falling or volatile markets due to rupee cost averaging. You buy more units when prices are low, balancing the cost.

2. Can I start a SIP and later switch to a lump sum investment?

Yes. You can start with a SIP and, once you have accumulated or received a large sum, add a lump sum to boost your investment.

3. How can I calculate returns from SIP and lump sum investments?

You can use online calculators or Excel formulas like XIRR for SIPs and CAGR for lump sum.

4. Which is more tax-efficient: SIP or lump sum?

Both are taxed similarly based on the type of mutual fund. However, SIPs have multiple investment dates, so tracking holding periods can be complex.

5. Is SIP suitable for short-term goals?

SIPs are better suited for long-term goals (5 years or more). For short-term goals, consider liquid or ultra-short-term funds.

6. Can I pause or stop SIP anytime?

Yes, most SIPs are flexible. You can pause, stop, or even increase your SIP amount depending on your financial situation.

7. What happens if the market crashes after my lump sum investment?

You may face short-term losses, but staying invested for the long term can help recover and gain.

Investing in mutual funds remains a popular strategy for wealth creation, offering diversification and professional management. As we navigate through 2025, selecting the right mutual funds is crucial to align with your financial goals and risk appetite. This comprehensive guide explores top-performing mutual funds across various categories, providing insights to help you make informed investment decisions.

Key Takeaways

Diversify Investments: Spread investments across various fund categories to mitigate risks.

Align with Goals: Choose funds that match your financial objectives and time horizon.

Monitor Performance: Regularly assess fund performance and make necessary adjustments.

Understand Costs: Be aware of expense ratios and their impact on returns.

Stay Informed: Keep abreast of market trends and fund manager strategies.

The Indian mutual fund industry has witnessed significant growth, with investors increasingly seeking avenues to maximize returns. In 2025, despite market volatility, certain mutual funds have demonstrated resilience and consistent performance. This guide delves into the best mutual funds to invest in, based on recent performance data and expert analyses.

Top Mutual Funds to Consider in 2025

Large Cap Funds

Large cap funds invest in companies with large market capitalization, offering stability and steady returns.(INDmoney)

Canara Robeco Bluechip Equity Fund: Known for its consistent performance and robust portfolio comprising blue-chip companies.

Mirae Asset Large Cap Fund: Offers a diversified portfolio with a focus on long-term capital appreciation.

HDFC Flexi Cap Fund: Provides flexibility to invest across market capitalizations, with a significant allocation to large-cap stocks.

Mid Cap Funds

Mid cap funds target medium-sized companies with high growth potential.(The Economic Times)

Axis Midcap Fund: Recognized for its strong track record and quality stock selection.

Kotak Emerging Equity Fund: Focuses on emerging companies poised for substantial growth.(INDmoney)

PGIM India Midcap Opportunities Fund: Offers a diversified portfolio with an emphasis on mid-sized companies.

Flexi Cap Funds

Flexi cap funds provide the flexibility to invest across large, mid, and small-cap stocks.(The Economic Times)

Parag Parikh Flexi Cap Fund: Known for its value investing approach and international diversification.

Mirae Asset Hybrid Equity Fund: Combines equity and debt instruments to balance risk and return.

Hybrid Funds

Hybrid funds invest in a mix of equity and debt instruments, aiming to balance risk and return.

SBI Equity Hybrid Fund: Offers a balanced approach with a mix of equity and fixed income securities.

ICICI Prudential Equity & Debt Fund: Focuses on generating long-term capital appreciation and income.

Sectoral/Thematic Funds

These funds focus on specific sectors or themes, offering higher returns with increased risk.

ICICI Prudential Infrastructure Fund: Invests in infrastructure-related companies, benefiting from government initiatives.

SBI PSU Fund: Targets public sector undertakings, capitalizing on their growth potential.

Factors to Consider Before Investing

Investment Goals: Define your financial objectives, whether it’s wealth creation, retirement planning, or buying a house.

Risk Appetite: Assess your tolerance for risk to choose appropriate fund categories.

Time Horizon: Determine your investment duration to align with fund performance cycles.

Fund Performance: Analyze historical returns, consistency, and fund manager expertise.

Expense Ratio: Consider the cost of managing the fund, as higher expenses can impact net returns.

Portfolio Diversification: Ensure the fund offers a diversified portfolio to mitigate risks.

1. How to Choose the Right Mutual Fund for Your Financial Goals?

Description: Explain goal-based investing and how to match mutual fund categories (debt, equity, hybrid, ELSS) with short-term, medium-term, and long-term goals.

Subtopics: Risk tolerance, time horizon, SIP vs. lump sum, growth vs. dividend options.

2. What Is SIP and Why Is It the Smart Way to Invest in 2025?

Description: Dive into Systematic Investment Plans—how they work, benefits, compounding power, and long-term wealth creation potential.

Subtopics: SIP calculators, monthly budget planning, best SIPs in equity/debt funds.

3. Is ELSS Still the Best Tax-Saving Mutual Fund in 2025?

Description: Explore Equity-Linked Savings Scheme (ELSS), its tax benefits under Section 80C, lock-in period, and top ELSS funds to invest in.

Subtopics: ELSS vs. PPF vs. NPS, best ELSS options, long-term return potential.

4. What Are Hybrid Mutual Funds and Are They Ideal for Conservative Investors?

Description: Guide on hybrid funds that combine equity and debt for balanced growth with moderate risk.

Subtopics: Types of hybrid funds (aggressive, conservative), ideal investor profile.

5. Which Are the Best Mutual Funds for Retirement Planning in 2025?

Description: Help readers build a retirement-focused portfolio using SIPs in equity, hybrid, and NPS-linked funds.

Investing in mutual funds in 2025 requires careful consideration of various factors, including market conditions, fund performance, and individual financial goals. By selecting funds that align with your objectives and risk profile, you can build a robust investment portfolio. Regularly reviewing and rebalancing your investments will help in achieving long-term financial success.

FAQs

1. What is the minimum amount required to start investing in mutual funds?

Most mutual funds allow investments starting from ₹500 through Systematic Investment Plans (SIPs).

2. Are mutual funds safe investments?

While mutual funds are subject to market risks, diversification and professional management help mitigate risks.

3. How are mutual fund returns taxed?

Taxation depends on the type of fund and holding period. Equity funds held for over a year attract Long-Term Capital Gains (LTCG) tax at 10% beyond ₹1 lakh.

4. Can I withdraw my investment anytime?

Open-ended mutual funds offer liquidity, allowing investors to redeem units at any time.

5. What is the difference between direct and regular mutual fund plans?

Direct plans have lower expense ratios as they are purchased directly from the fund house, while regular plans involve intermediaries and higher costs.

6. How do I choose the right mutual fund?

Consider factors like investment goals, risk tolerance, fund performance, and expense ratio.

7. Is it better to invest through SIP or lump sum?

SIPs promote disciplined investing and average out market volatility, while lump sum investments may be suitable when markets are low.

In 2025, achieving financial stability requires smart investing. With economic shifts, rising inflation, and evolving markets, choosing the right investment avenues is more important than ever. Whether you’re a beginner or a seasoned investor, this list highlights the top 10 best investment options in 2025 that offer both safety and strong growth potential.

1. Systematic Investment Plans (SIP) in Mutual Funds

In today’s fast-paced financial environment, Systematic Investment Plans (SIPs) have emerged as one of the most disciplined and effective ways to invest in mutual funds. For individuals seeking long-term wealth creation without the stress of timing the market, SIPs offer a consistent, flexible, and smart investment route.

✅ What is SIP?

A Systematic Investment Plan (SIP) allows an investor to invest a fixed amount in a mutual fund scheme at regular intervals — typically monthly or quarterly. Unlike lump sum investments, SIPs help you average out your purchase cost over time, thanks to a principle known as rupee cost averaging. This strategy makes SIPs particularly appealing during market volatility.

💡 Why Choose SIP in 2025?

In 2025, the financial market is characterized by growing investor participation, digital accessibility, and increased awareness about wealth creation. SIPs align perfectly with the needs of the modern investor:

Low entry barrier – Start investing with as little as ₹500 per month

No need to time the market – You invest in both highs and lows, averaging your costs

Compound growth – SIPs benefit from the power of compounding, helping your wealth multiply steadily

Digital convenience – Automated investments through apps and platforms make SIPs hassle-free

📈 Types of Mutual Funds for SIP

There are various categories of mutual funds available for SIPs, catering to different risk appetites and goals:

Equity Mutual Funds – Best for long-term growth, though slightly riskier. Ideal for 5+ year investments.

Debt Mutual Funds – Suitable for conservative investors, offering stable returns with lower risk.

Hybrid Funds – A mix of equity and debt, offering a balanced approach.

ELSS (Equity Linked Savings Scheme) – Offers tax benefits under Section 80C and is ideal for salaried individuals looking to save taxes.

💰 Benefits of SIP Investment

Disciplined savings: Encourages regular saving habits without lump-sum pressure.

Flexible investing: You can increase, decrease, pause, or stop your SIP anytime.

Diversification: Mutual funds diversify across stocks, sectors, and markets, minimizing risks.

Goal-based planning: SIPs help in achieving specific goals like education, marriage, or retirement.

🔢 Example of SIP Growth (Illustrative)

If you invest ₹5,000 per month in a SIP for 10 years at an average annual return of 12%, your investment will grow to over ₹11.6 lakhs, out of which ₹6 lakhs is your contribution, and the rest is profit through compounding.

Monthly SIP

Duration

Estimated Return (12%)

Total Value

₹5,000

10 years

₹11.6 lakhs

₹6 lakhs invested + ₹5.6 lakhs return

(Note: Returns are market-linked and not guaranteed.)

📅 Best Time to Start SIP? Now!

The best part of SIP is: you don’t need to wait. The earlier you start, the more time your money gets to grow. SIPs are especially suited for young professionals, salaried employees, and anyone with a steady income.

📲 How to Start SIP in 2025?

Starting a SIP is easier than ever:

Choose a mutual fund platform (Groww, Zerodha Coin, Paytm Money, etc.)

Complete your KYC online

Select a fund based on your risk profile

Set your SIP amount and date

Enable auto-debit from your bank account

2. Public Provident Fund (PPF)

The Public Provident Fund (PPF) continues to be one of the most trusted and safest long-term investment options for Indian investors in 2025. Backed by the Government of India, PPF offers a perfect mix of guaranteed returns, tax savings, and capital protection, making it ideal for conservative and risk-averse individuals.

🏦 What is PPF?

PPF is a long-term savings scheme introduced by the Indian government to promote regular savings among citizens. It comes with a 15-year lock-in period and earns a fixed interest rate that is reviewed quarterly by the Ministry of Finance. As of early 2025, the PPF interest rate stands at approximately 7.1% per annum (compounded annually).

📋 Key Features of PPF

Tenure: 15 years (extendable in 5-year blocks after maturity)

Minimum Investment: ₹500 per year

Maximum Investment: ₹1.5 lakh per financial year

Tax Benefits: Tax deduction under Section 80C, and interest + maturity amount are tax-free

Interest: Compounded annually and credited on March 31 every year

🔐 Safety and Stability

PPF is a sovereign-backed investment, meaning your money is as safe as a government deposit. Unlike market-linked investments such as mutual funds or equities, PPF offers guaranteed returns without any market risks. It’s especially suitable for individuals looking to create a secure retirement corpus or save for their children’s future.

💡 Benefits of Investing in PPF

Triple Tax Exemption (EEE Status) PPF falls under the Exempt-Exempt-Exempt category:

Contribution qualifies for deduction under Section 80C (up to ₹1.5 lakh)

Interest earned is tax-free

Maturity proceeds are tax-free

Compound Growth The annual compounding of interest ensures your savings grow faster, especially if you start early and remain consistent.

Loan and Withdrawal Facility

You can take a loan against PPF from the 3rd to the 6th financial year.

Partial withdrawals are allowed from the 7th financial year onwards, subject to conditions.

Ideal for Long-Term Goals Planning for retirement, children’s education, or marriage? PPF is an excellent tool for goal-based investing with peace of mind.

🧮 Example of PPF Returns

If you invest ₹1.5 lakh per year for 15 years at an interest rate of 7.1%, your total investment of ₹22.5 lakhs can grow to approximately ₹40.7 lakhs on maturity — completely tax-free!

Year

Annual Investment

Total Corpus (Approx.)

15

₹1.5 lakh

₹40.7 lakhs

(Note: Returns are based on current interest rates and may change.)

📝 Who Should Invest in PPF?

Salaried professionals looking for tax-saving options

Invest early in the financial year (preferably in April) to maximize yearly compounding.

Invest the full ₹1.5 lakh if possible, to gain full tax benefits and higher returns.

Use PPF as a foundation for your retirement portfolio along with EPF/NPS.

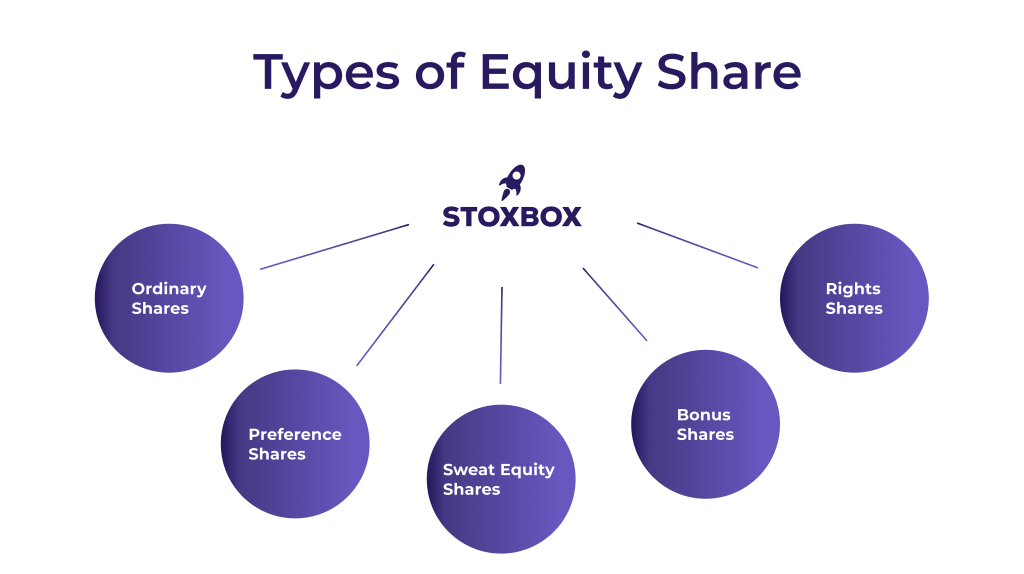

3. Stocks and Equity Shares

For high-risk appetite investors, the stock market offers unmatched growth. With the rise of digital trading apps, investing in top-performing Indian stocks has become easier and more accessible in 2025.

Why invest?

Potential for high returns

Dividend income + capital appreciation

Great for long-term wealth building

📊 What Are Equity Shares?

Equity shares, or stocks, are units of ownership in a publicly listed company. When you buy shares of a company, you become a part-owner (shareholder) and are entitled to:

A share in the company’s profits (dividends)

Voting rights (in some cases)

Capital appreciation (when stock prices rise)

Stocks are traded on recognized stock exchanges like NSE (National Stock Exchange) and BSE (Bombay Stock Exchange).

📈 Benefits of Investing in Stocks

High Growth Potential Equities have historically beaten inflation and delivered superior returns over long-term periods.

Liquidity Stocks are highly liquid — you can buy/sell them easily during trading hours.

Dividend Income Many companies share their profits with shareholders in the form of dividends.

Ownership and Transparency As a shareholder, you have voting rights and access to public financial reports.

Wide Choice of Sectors You can invest in banks, tech, pharma, energy, FMCG, and other high-growth sectors.

4. Real Estate

🏡 What is Real Estate Investment?

Real estate investment involves purchasing physical property—residential, commercial, or land—with the objective of earning income or achieving capital appreciation over time. There are also indirect ways to invest in real estate, such as Real Estate Investment Trusts (REITs), which are becoming increasingly popular in India.

🏙️ Types of Real Estate Investments

Residential Property

Apartments, villas, and houses bought for resale or rental income.

High demand in urban and semi-urban areas due to population growth.

Commercial Property

Office spaces, retail shops, and warehouses.

Generally more expensive but offer higher rental yields than residential units.

Land or Plots

Undeveloped land in growing areas can offer high appreciation over time.

REITs (Real Estate Investment Trusts)

Suitable for small investors.

Offers dividend income and liquidity through stock exchanges.

💰 Why Invest in Real Estate in 2025?

The Indian real estate market is showing strong signs of revival post-pandemic. Government reforms, improved infrastructure, and increased urbanization are contributing to steady growth in both residential and commercial sectors. Key reasons to invest now include:

Appreciation potential in tier 1 and tier 2 cities

Stable rental income from residential/commercial properties

Government incentives like PMAY (Pradhan Mantri Awas Yojana), RERA compliance, and GST benefits

Rise of REITs providing easier access to real estate with small capital

📈 Benefits of Real Estate Investment

Tangible Asset Unlike stocks or mutual funds, real estate is a physical asset that you can see and manage.

Rental Income A properly located property can generate monthly rental income, offering financial stability.

Value Appreciation Over the long term, property prices tend to increase, especially in growing localities.

Tax Advantages

Tax deductions on home loan interest under Section 24

Deductions on principal repayment under Section 80C

Depreciation benefits for commercial properties

Hedge Against Inflation Property values and rent typically rise with inflation, preserving your purchasing power.

⚠️ Risks and Considerations

High Entry Cost: Requires significant capital for purchase, registration, and maintenance.

Low Liquidity: Unlike stocks or mutual funds, it may take weeks or months to sell property.

Market Fluctuations: Prices can stagnate or fall based on location, demand, or economic conditions.

Legal and Regulatory Issues: Must ensure proper documentation, approvals, and RERA compliance.

5. Fixed Deposits (FDs)

Despite newer investment tools, fixed deposits are still relevant in 2025, especially for low-risk investors. Many banks offer interest rates up to 7.5% per annum, and FDs are now more flexible with online management.

💰 What is a Fixed Deposit?

A Fixed Deposit is a financial instrument provided by banks and non-banking financial companies (NBFCs) where you can invest a lump sum of money for a fixed tenure at a predetermined interest rate. At the end of the tenure, you receive your original investment along with the accrued interest.

FDs offer guaranteed returns, unaffected by market fluctuations, making them an ideal investment for short- to medium-term financial goals.

Why invest?

Stable, guaranteed returns

Short to medium-term horizon

Low risk and easy liquidity

✅ Benefits of Investing in Fixed Deposits

Guaranteed Returns The interest rate is fixed at the time of investment, ensuring predictable earnings.

Capital Safety FDs are among the safest investment options, especially when placed with government-backed or reputed banks.

Flexible Tenures You can choose tenures ranging from 7 days to 10 years depending on your financial needs.

Loan Facility Many banks allow you to take a loan or overdraft against your FD, up to 90% of its value.

Senior Citizen Advantage Senior citizens get additional interest rates and are eligible for tax-saving FDs under specific schemes.

Tax-Saving Options 5-year tax-saving FDs qualify for deduction under Section 80C (up to ₹1.5 lakh annually).

6. National Pension Scheme (NPS)

NPS is perfect for long-term retirement planning. It offers both equity and debt exposure, and allows you to build a sizable retirement corpus with tax benefits under 80CCD.

🧾 What is NPS?

The National Pension Scheme is a voluntary, defined-contribution retirement savings plan regulated by the Pension Fund Regulatory and Development Authority (PFRDA). Under NPS, subscribers invest regularly in a mix of equity, corporate debt, government bonds, and alternative assets, based on the selected asset allocation.

At retirement (age 60), investors can withdraw up to 60% of the corpus tax-free, while 40% must be used to buy an annuity to receive a regular monthly pension.

Why invest?

Low management charges

Partial tax exemption at maturity

Annuity + lump sum payout options

📈 Key Features of NPS

Low management cost (around 0.01% annually)

Flexible asset allocation: Equity (up to 75%), Corporate Bonds, Government Securities

Choice of fund managers (HDFC, SBI, LIC, ICICI, UTI, etc.)

Auto and Active investment choices to suit risk appetite

Online account access through NSDL or Karvy

7. Gold Investments (Digital & Physical)

Gold has always been a hedge against inflation. In 2025, digital gold, sovereign gold bonds (SGBs), and gold ETFs are gaining popularity for being secure and easy to trade.

🏅 What is Gold Investment?

Gold investment refers to the process of purchasing gold in various forms, such as coins, bars, jewelry, digital gold, or through Gold ETFs (Exchange-Traded Funds), to generate profits either from capital appreciation or by earning income from gold-backed financial products.

Gold is widely viewed as a tangible asset with long-term value, historically retaining purchasing power even during times of economic uncertainty.

Why invest?

Hedge against market volatility

SGBs offer interest + gold price appreciation

Liquidity through digital platforms

8. REITs (Real Estate Investment Trusts)

REITs are a great alternative to buying property directly. They let you invest in commercial real estate and earn dividends.

Why invest?

Low capital requirement

Regular income through dividends

Exposure to real estate without ownership hassles

📈 Types of REITs

Equity REITs:

These REITs own and operate income-generating real estate, such as office buildings, shopping malls, and residential complexes.

Investors benefit from the rental income and property value appreciation.

Mortgage REITs (mREITs):

These REITs invest in real estate mortgages or mortgage-backed securities (MBS).

mREITs make money by earning the difference between the cost of borrowing and the interest they receive from the mortgages they hold.

Hybrid REITs:

A combination of both equity and mortgage REITs, offering investors exposure to both real estate properties and mortgage assets.

Public Non-Listed REITs:

These are REITs that are registered with the SEC but are not traded on stock exchanges.

They can provide a higher yield but are less liquid than publicly traded REITs.

9. Cryptocurrency (With Caution)

Crypto assets are still volatile, but regulated platforms and stablecoins have made them more appealing in 2025. While not for everyone, some investors allocate a small part of their portfolio to crypto for diversification.

💡 What is Cryptocurrency?

Cryptocurrency is a form of digital or virtual currency that uses cryptography for security. Unlike traditional currencies issued by governments (such as the dollar or euro), cryptocurrencies operate on blockchain technology, which is a decentralized and distributed ledger across a network of computers. This means cryptocurrencies are not controlled by any central authority, such as a government or bank, making them resistant to inflation and government interference.

The most well-known cryptocurrencies include:

Bitcoin (BTC): The first and most valuable cryptocurrency, often considered a store of value.

Ethereum (ETH): A platform that allows developers to build decentralized applications and execute smart contracts.

Binance Coin (BNB), Ripple (XRP), Cardano (ADA), and many other altcoins have gained significant attention in the market.

Why invest?

High growth potential

Decentralized and global

Suitable for tech-savvy investors

🧮 The Risks of Cryptocurrency Investment

While the rewards of cryptocurrency investment can be high, the risks are equally significant. It’s crucial to approach these investments with caution and awareness of the dangers involved.

Volatility: Cryptocurrency prices are highly volatile. A 10–20% price swing in a single day is not uncommon. For example, Bitcoin’s price can go from $40,000 to $30,000 in a matter of hours and back up again, which can be disorienting for unprepared investors. While the potential for large returns exists, this volatility can also lead to substantial losses.

Regulatory Uncertainty: Governments worldwide are still grappling with how to regulate cryptocurrencies. Countries like China have imposed strict bans on crypto trading, while others, like the United States and India, are working on creating frameworks for taxation and regulation. Regulatory changes can affect cryptocurrency prices and availability, potentially leading to market crashes.

Security Risks: Cryptocurrency investments are only as secure as the storage methods you choose. Hacks and fraudulent schemes are common in the crypto world. For example, exchanges like Mt. Gox have been hacked in the past, resulting in millions of dollars in losses. Investing in hardware wallets (cold storage) rather than leaving coins on exchanges (hot wallets) can minimize risk.

Lack of Consumer Protections: Unlike traditional investments like stocks or bonds, cryptocurrencies lack the regulatory oversight that protects consumers. If you lose access to your crypto wallet, for instance, there is often no way to recover your funds. Additionally, fraudulent schemes like Ponzi schemes and pump-and-dump scams are prevalent in the crypto market.

Market Manipulation: The crypto market, particularly in smaller altcoins, can be susceptible to market manipulation by large holders (often referred to as “whales”). A large investor can manipulate the market by buying or selling massive amounts of a specific cryptocurrency, which can artificially inflate or deflate its price.

10. ULIPs (Unit Linked Insurance Plans)

ULIPs offer the dual benefit of investment + life insurance. They are best suited for long-term investors looking for both protection and wealth creation.

Why invest?

Tax-free returns under Section 10(10D)

Life cover included

Flexible fund switching

💡 What is a ULIP?

A Unit Linked Insurance Plan (ULIP) is a product offered by life insurance companies, where the policyholder pays a premium, and the money is then invested in various market-linked instruments (like equity, debt, or hybrid funds) based on the policyholder’s risk tolerance and investment preferences. A portion of the premium is allocated to life insurance coverage, while the remainder is invested in units of a selected fund, such as equity or debt funds.

The value of the investment is subject to market performance, and the funds grow or decline in value based on the performance of the underlying assets. This gives the policyholder the potential to build wealth over time while also receiving life cover.

Choosing the right investment in 2025 depends on your risk appetite, time horizon, and financial goals. A balanced portfolio combining fixed returns, market-linked assets, and tax-saving tools can help you achieve guaranteed and sustainable growth. Always research or consult a financial advisor before making investment decisions.

Investing money is a powerful way to build wealth, secure your financial future, and achieve life goals. But if you’re just starting out, the process can feel overwhelming. With thousands of investment options, financial jargon, and market uncertainties, knowing where and how to start investing is the key to success.

This beginner’s guide is designed to simplify everything—from understanding basic investment concepts to selecting the right tools and strategies. Let’s break it down into practical steps so you can begin your investment journey with confidence.

Key Takeaways

Start early to benefit from compounding.

Set clear financial goals before investing.

Begin with simple investments like mutual funds and ETFs.

Diversify your portfolio to reduce risk.

Avoid common mistakes like emotional investing and lack of research.

Use SIPs to build disciplined investing habits.

Review and adjust your investments regularly.

Why Should You Start Investing Early?

1. Power of Compounding

One of the biggest advantages of starting early is compound interest. This means you earn interest not just on your initial investment, but also on the interest it accumulates over time.

Example: Investing ₹1,00,000 at 10% annually for 20 years will become ₹6,72,750. But if you wait 10 years to start, it becomes only ₹2,59,374.

2. Achieving Long-Term Goals

Whether it’s retirement, buying a house, or funding your child’s education, early investment helps you reach these goals with ease.

3. Risk Management

You can take calculated risks when you have time on your side, allowing recovery from market fluctuations.

Understanding Basic Investment Concepts

1. Risk and Return

Every investment involves some level of risk. Higher returns usually come with higher risk. Learn to balance the two according to your goals and comfort.

2. Diversification

Never put all your money in one place. Spread it across various assets like stocks, bonds, and mutual funds to reduce overall risk.

3. Liquidity

How quickly you can convert your investment into cash matters. Stocks are more liquid than real estate, for example.

4. Inflation

Your investment should at least beat inflation. If inflation is 6% and your savings grow at 4%, you’re losing money in real terms.

Investing doesn’t have to be intimidating. With the right knowledge, clear goals, and a long-term mindset, even beginners can create strong portfolios that deliver consistent returns. The most important step is to start. Don’t wait for the perfect moment—begin today, even with a small amount.

Remember, the earlier you start investing, the more you benefit from compounding and long-term market growth. Use the tools and resources available, stay disciplined, and keep learning along the way.

FAQs

1. How much money do I need to start investing?

You can start with as little as ₹500/month using SIPs in mutual funds. Many platforms have no minimum balance.

2. Is investing in stocks safe for beginners?

Yes, if done wisely. Start with blue-chip stocks or equity mutual funds. Avoid day trading or penny stocks.

3. How do I choose the best mutual fund?

Look for funds with consistent returns, low expense ratios, and a good fund manager. Use apps that rate mutual funds.

4. What’s the difference between saving and investing?

Saving is keeping money safe (like in a bank). Investing involves putting money into assets that can grow over time.

5. Can I lose money when I invest?

Yes. Every investment carries some risk. However, long-term investing in quality assets tends to yield positive returns.

6. How long should I invest to see good returns?

At least 3–5 years for mutual funds and stocks. Longer duration reduces volatility and increases the potential for gains.

7. Should I hire a financial advisor?

Not necessary for everyone, but helpful if you’re dealing with large sums, multiple goals, or lack the time and knowledge.

Investing is one of the most effective ways to grow wealth, achieve financial goals, and build a secure future. Whether you’re planning for retirement, buying a home, or simply looking to generate passive income, choosing the right investment plan is crucial. While some investments offer safety and stability, others are designed to generate high returns—often with higher risk. This guide will explore the best investment plans for high returns, including traditional and modern options, along with expert insights to help you make informed decisions.

Key Takeaways

High returns come with high risk—know your risk appetite.

Stocks and mutual funds remain top choices for long-term high returns.

Cryptocurrencies and startups offer massive returns but require caution.

Diversification is crucial—don’t put all your eggs in one basket.

Always align investments with your financial goals and timeline.

Understanding Investment Returns

Investment returns refer to the gains or losses made on an investment over time. Returns can be in the form of:

Capital appreciation (increase in value of an asset)

Dividends (regular payouts from stocks or mutual funds)

Interest income (from fixed income or lending-based investments)

Rental income (in the case of real estate)

Returns are often calculated as a percentage of the initial investment and can vary significantly based on the type of asset, market conditions, and time horizon.

Key Factors to Consider Before Investing

Before diving into high-return investments, it’s crucial to evaluate:

1. Your Financial Goals

Are you investing for short-term gains or long-term wealth? High-return investments often require a longer time horizon.

2. Risk Appetite

Investments with higher returns generally come with higher risks. Assess how much volatility and potential loss you can tolerate.

3. Liquidity

Can you access your money when needed? Some investments lock in capital for long durations.

4. Tax Implications

Understand how your returns will be taxed—some investments may incur capital gains tax or income tax.

5. Diversification Needs

Spreading risk across multiple assets reduces the chance of loss.

Top High-Return Investment Plans

1. Stock Market Investments

a. Individual Stocks

Investing in equities has historically offered high long-term returns. Picking the right companies can lead to significant capital appreciation.

Average annual return: 10%–15%

Best for: Long-term investors, those with risk tolerance

b. Growth Stocks

These are companies expected to grow earnings rapidly.

Examples: Tech firms, startups

Potential for very high returns (20%+), but also high volatility

2. Mutual Funds

a. Equity Mutual Funds

These funds invest in diversified stocks and are professionally managed.

Offers tax benefits under Section 80C in India and has a 3-year lock-in period.

High returns + tax-saving = dual advantage

3. Real Estate

Investing in property can yield high returns through both capital appreciation and rental income.

Returns: 8%–12% (location-dependent)

Ideal for: Long-term investors with large capital

Pros:

Tangible asset

Hedge against inflation

Cons:

Low liquidity

High transaction costs

4. Cryptocurrencies

Although volatile, cryptocurrencies like Bitcoin and Ethereum have delivered astronomical returns over the past decade.

Returns: 30%+ annually (varies wildly)

Notable coins: BTC, ETH, Solana

Best for: High-risk appetite and tech-savvy investors

Caution: Regulatory risks and extreme volatility make this a high-risk category.

5. Peer-to-Peer Lending

Platforms like LendingClub or Prosper allow you to lend money directly to borrowers and earn interest.

Returns: 10%–15%

Risk: Borrower default, but platforms often vet borrowers

6. REITs (Real Estate Investment Trusts)

REITs offer a way to invest in real estate without buying property.

Returns: 8%–12%

Pros: High dividends, publicly traded, diversified

Cons: Sensitive to interest rates

7. Small-Cap Funds

These mutual funds invest in small-cap companies with high growth potential.

Returns: 15%–25% (historically)

Risk: Higher volatility than large-cap funds

Suitable for: Aggressive investors looking for long-term growth.

8. Startup Investing & Angel Investing

Invest in early-stage companies with innovative ideas. While 90% of startups fail, successful ones can return 10x–100x your investment.

Returns: Potentially 1000%+

Suitable for: Wealthy investors with access to vetted startups

Risk vs. Return: Striking the Right Balance

Every investment involves a risk-return tradeoff. To achieve high returns, you must accept some level of risk. Here’s a basic breakdown:

Investment Type

Return Potential

Risk Level

Stocks

High

High

Mutual Funds

Moderate-High

Medium

Real Estate

Medium

Medium

Crypto

Very High

Very High

P2P Lending

High

High

REITs

Medium

Low-Medium

Tips:

Use the 80/20 rule: 80% in stable investments, 20% in high-risk/high-return ones.

Rebalance your portfolio annually.

How to Diversify for High Returns

1. Mix Asset Classes

Combine stocks, mutual funds, real estate, and crypto for a well-rounded portfolio.

2. Geographic Diversification

Invest in international markets to reduce country-specific risks.

3. Sectoral Diversification

Invest across sectors—tech, healthcare, finance, energy—to spread risk.

How to Build a High-Return Investment Portfolio in 2025

Description: Step-by-step guide to building a diversified investment portfolio with a focus on maximizing returns. Covers asset allocation, risk management, tools, and platforms.

Subtopics:

Importance of diversification

Equity vs. alternative investments

Rebalancing strategies

Sample portfolios for different risk levels

Is Real Estate Still a High-Return Investment in 2025?

Description: In-depth analysis of real estate’s current ROI potential. Includes trends like REITs, rental income, flipping, and commercial vs. residential investment.

Subtopics:

Regional real estate trends

Tax benefits

Risk factors (vacancy, regulation)

Real estate vs. stock market returns

Top 10 Mutual Funds That Deliver High Returns (Updated 2025)

Description: A data-driven guide to the best-performing mutual funds for aggressive investors, with analysis, past returns, and future outlook.

Subtopics:

Fund performance comparisons

SIP vs. lump sum investment

Risk-adjusted returns

Expense ratios and fund manager reputation

Cryptocurrency Investment for High Returns: Is It Worth the Risk?

Description: A balanced overview of crypto investing for high returns, covering major coins, altcoins, DeFi, and staking.

Subtopics:

Market volatility

Regulatory risks

Wallets and exchanges

Historical ROI of Bitcoin, Ethereum

High-Return Investment Plans with Tax Benefits

Description: Explore investment options that offer both high returns and tax-saving advantages.

Subtopics:

ELSS (Equity Linked Saving Scheme)

NPS (National Pension Scheme)

PPF vs. ULIPs

Tax harvesting techniques

Small-Cap vs. Large-Cap: Which Offers Better Long-Term Returns?

Description: Compare the ROI, volatility, and risk of investing in small-cap vs. large-cap stocks and funds.

Subtopics:

Historical performance

Ideal time horizon

Sectoral trends in small-cap

Investing via mutual funds vs. direct equity

Passive Income Investments with High Returns

Description: Focus on investments that generate recurring income while appreciating in value.

Subtopics:

Dividend-paying stocks

Rental properties

REITs and P2P lending

Royalties and digital assets

Top Investment Mistakes That Reduce Your Returns

Description: Discuss common investor errors and how they can impact high-return strategies.

Subtopics:

Emotional investing

Timing the market

Lack of research

Over-diversification

AI and Robo-Advisors: The Future of High-Return Investing?

Description: Review how AI-driven platforms help investors earn better returns with less effort.

Subtopics:

Best robo-advisor platforms

Algorithmic portfolio optimization

Risk profiling using AI

Pros and cons of automation

Best High-Return Investment Strategies for Millennials and Gen Z

Description: Tailored investment plans for younger Investors with higher risk Appetite and longer time horizon.

Subtopics:

Cryptocurrency and NFTs

Growth stocks and thematic funds

Socially responsible investing (SRI)

Financial independence and early retirement (FIRE)

Achieving high returns from your investments requires more than luck—it demands a clear strategy, strong research, and disciplined execution. From stocks and mutual funds to cryptocurrencies and real estate, various avenues can deliver excellent returns over time. However, higher returns often mean greater risk. Understanding this balance is the key to long-term success. Start small, diversify wisely, and stay consistent.

FAQs

1. What is the safest high-return investment?

While no investment is 100% safe, mutual funds and REITs offer relatively high returns with moderate risk.

2. How much should I invest for high returns?

Ideally, invest 15–25% of your portfolio in high-return options, depending on your risk appetite.

3. Can I get high returns with low risk?

It’s rare. However, diversified mutual funds and long-term equity investments offer a good balance.

4. Are cryptocurrencies a good long-term investment?

Cryptos can deliver high returns, but they are highly volatile. Only invest what you can afford to lose.

5. How long should I stay invested for high returns?

Typically, a 5–10 year horizon is ideal for maximizing returns in equity and real estate.

6. What is the return potential of P2P lending?

Returns range from 10%–15%, but risk of default is high.

7. How can I reduce risk while investing?

Diversify

Invest for the long term

Avoid herd mentality

Use SIPs (Systematic Investment Plans) for equity exposure